A reverse mortgage is a unique type of loan that lets a homeowner receive monthly payouts from a lender, without having to make any payments. But it’s not uncommon for homeowners who choose a reverse mortgage to eventually decide it isn’t right for them anymore.

If you’re wondering how to get out of a reverse mortgage, the good news is that you usually can — and there are plenty of alternatives available if you still want to borrow against your home equity.

Reverse mortgages work differently from traditional (“forward”) mortgages. With a traditional mortgage, you borrow money to purchase a home and make monthly payments until the loan is paid in full. But when a homeowner takes out a reverse mortgage, instead of making payments, they receive payouts from the lender based on how much equity is in the home.

As a traditional mortgage progresses, a homeowner builds home equity (the portion of the home they own outright) and the loan balance decreases. But as a reverse mortgage continues, the borrower’s home equity decreases and the amount they owe the lender increases. Interest and fees will also accrue, causing the loan balance to grow.

A reverse mortgage doesn’t have to be paid off until the last surviving borrower passes away, sells the property or no longer lives there. In most cases, homeowners or their heirs need to sell the home to satisfy the loan.

![]()

Learn more about the pros and cons of reverse mortgages.

The most common type of reverse mortgage is a home equity conversion mortgage (HECM), which is backed by the Federal Housing Administration (FHA).

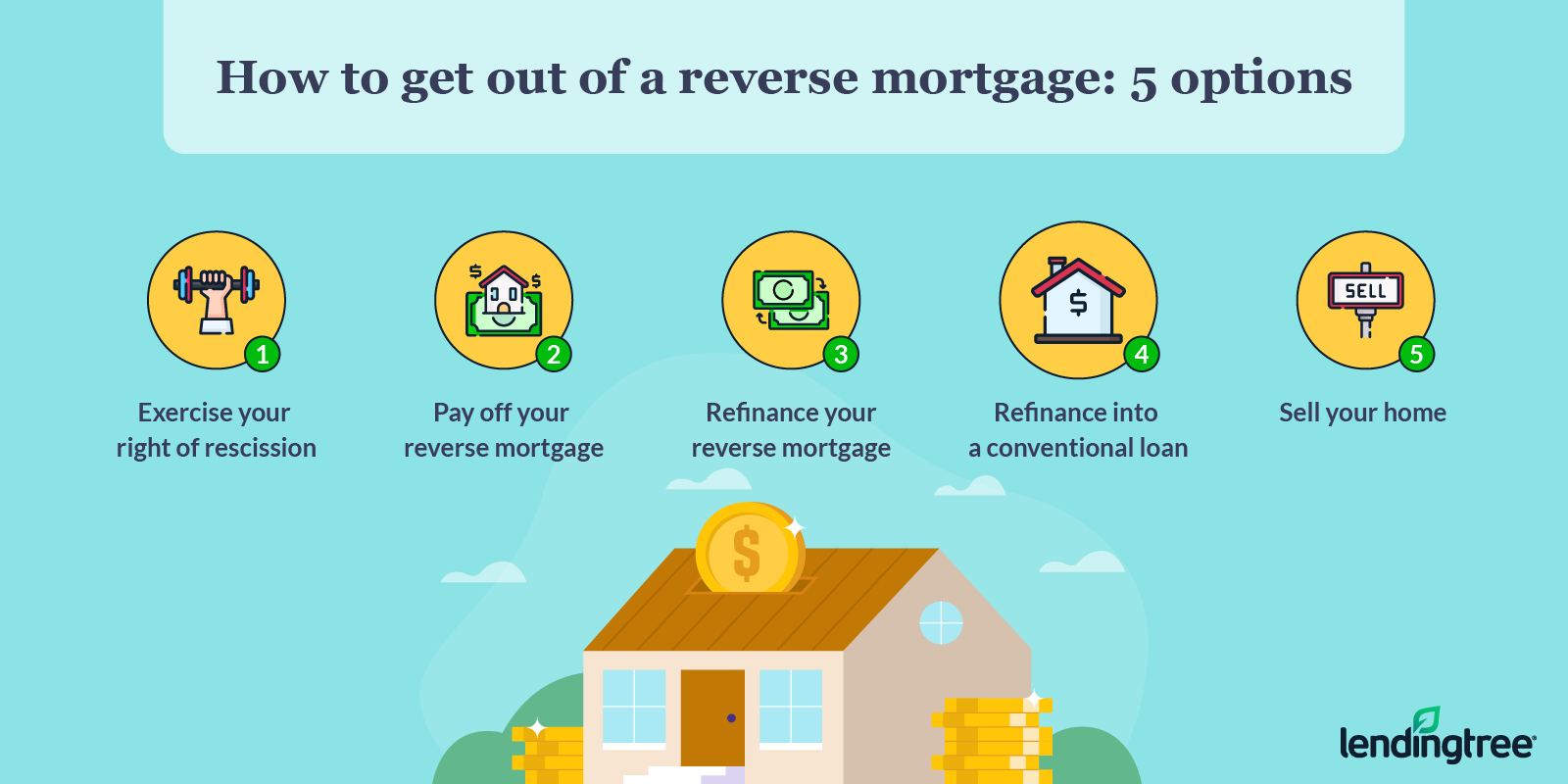

If you’re wondering how to get out of a reverse mortgage, your situation has likely changed since you took one out and now you’re looking for alternatives. We’ve provided five options, but the right choice for you will depend on how long ago you first borrowed the loan and your overall financial situation:

If you regret your reverse mortgage within a matter of days after you’ve signed the paperwork, you can take advantage of the “right of rescission” period.

The right of rescission is a consumer protection that lets you change your mind for any reason, without penalty, up to three business days after signing the loan agreement. To cancel your reverse mortgage via this option, you’ll need to inform your lender in writing. The lender has to return any money you’ve paid for the financing within 20 days.

Paying off the loan balance in full is another simple way to get out of a reverse mortgage.

In most cases, you can do this at any time without incurring a prepayment penalty.

If you have enough cash on hand to pay off the loan, you’re in great shape — but what if you don’t? Typically, you’d need to seek another form of financing that can pay off the reverse mortgage balance. This could be a cash-out refinance, home equity loan or home equity line of credit (HELOC), or even a personal loan.

![]()

Read our comparison of cash-out refinances vs. HELOCs vs. home equity loans.

Another option is refinancing into a new reverse mortgage with better terms. For example, if mortgage interest rates have decreased significantly since taking out your original reverse mortgage, it might benefit you to refinance. With this path, you’ll pay less interest over the life of the loan.

![]()

Learn more about how to refinance your mortgage.

If you no longer need the additional income that a reverse mortgage provides and can afford to make a monthly mortgage payment, you can refinance your reverse mortgage with a conventional loan. You might consider this path if you’re looking to preserve your home equity and avoid potential reverse mortgage problems for your heirs.

However, this option might not be feasible if you took out the reverse mortgage because you needed additional income to cover your monthly mortgage expenses or pay for home repairs.

Another way to get out of a reverse mortgage is to sell your home. The sale proceeds usually satisfy the loan even if the reverse mortgage is underwater. In that case, borrowers typically sell the home for the lesser of the loan balance or 95% of the property’s appraised value. Because HECMs are insured by the federal government, the mortgage insurance built into the loan takes care of the remaining balance.

→ Seek help from a HUD-approved counselor. If you have concerns about your reverse mortgage, speak to a reverse mortgage counselor. In addition to discussing the loan repayment process, the counselor can also help you locate other federal or state resources, such as SNAP or other government programs.

→ Review your long-term plans. Know what goals you want to prioritize, including whether you wish to remain in the home long term or pass the property to your heirs.

→ Consider the costs. Keep in mind that any course of action you take will come at a cost. Refinancing your existing loan with either a conventional mortgage or a new reverse mortgage will entail refinance closing costs.

→ Communicate with your lender. At the first sign of trouble, reach out to your lender to discuss the reverse mortgage problems you’re facing. They can help you understand your options.

→ Make partial payments. Even if you can’t afford to repay your reverse mortgage in a lump sum, you might consider making partial prepayments now to reduce the amount owed later on. Most reverse mortgages allow partial prepayments without charging a penalty, but be sure to talk to your loan servicer about your prepayment options and confirm how those payments will be applied.

→ Submit a complaint

![]()

Think a refinance may be right for you? Browse today’s refinance rates and best lenders to get started.